When tackling debt, you might fall into common traps that hinder your progress. Ignoring interest rates or just making minimum payments can prolong your struggle. Failing to create a budget leaves you disorganized, while neglecting emergency savings can lead to more debt. Using credit cards for everyday expenses and not communicating with creditors adds to your financial woes. Also, underestimating the importance of financial education can keep you in the dark. There’s more to uncover about these pitfalls.

Key Takeaways

- Ignoring interest rates and making only minimum payments can prolong debt repayment and increase overall costs due to accumulating interest.

- Failing to create a budget leads to chaotic debt management, missed payments, and late fees.

- Neglecting emergency savings forces reliance on credit for unexpected expenses, potentially increasing debt.

- Using credit cards for daily expenses can lead to overspending and hinder debt repayment efforts.

- Not communicating with creditors may result in missed payments and increased debt from late fees and interest charges.

Ignoring the Interest Rates

What it Looks like:

Ignoring the interest rates on your debts can lead to a misleading sense of progress. Many individuals focus solely on making minimum payments or paying off smaller debts first, without considering the interest rates associated with each account. For example, a person might prioritize paying off a credit card with a lower balance but a higher interest rate, while continuing to carry a larger balance on a card with a markedly lower interest rate. This approach can result in paying more interest over time, ultimately prolonging the journey to being debt-free and increasing the financial strain on the debtor.

Why It’s Smart:

Understanding and prioritizing debts based on interest rates can save you a substantial amount of money. By targeting high-interest debts first, you can reduce the overall amount of interest paid, which means more of your payment goes toward the principal balance. This strategy, often referred to as the avalanche method, allows you to eliminate debts more efficiently. Additionally, by keeping an eye on interest rates, you can also make informed decisions about whether to consolidate debt or seek lower-interest financing options, further hastening your path to financial freedom.

Things to Be Aware of:

It’s essential to regularly review the interest rates on all your debts, as they can change over time, especially with variable-rate loans or credit cards. Additionally, be cautious of promotional rates that may expire after a certain period, which can lead to a spike in your monthly payments. Moreover, remember that while focusing on high-interest debts is vital, it’s also important to maintain a balanced approach that keeps you motivated. Allowing smaller debts to linger without a strategy can lead to discouragement and may derail your overall debt repayment plan.

Making Only Minimum Payments

What it Looks like:

When individuals opt to make only the minimum payments on their debts, it often appears as a manageable strategy in the short term. Minimum payments are usually calculated as a small percentage of the outstanding balance or a fixed dollar amount, which can create a false sense of security. Borrowers may feel relief when they see their accounts remain in good standing and avoid late fees. However, this approach can lead to prolonged debt repayment timelines and substantial interest accumulation, resulting in a much larger amount paid over the life of the debt than initially anticipated.

Why It’s Smart:

Making only minimum payments may seem like a practical choice, especially during financially tight times. It allows individuals to maintain cash flow for other expenses, making it easier to manage day-to-day finances. Additionally, it can help to prevent defaulting on loans, protecting one’s credit score from potential damage. However, while it may seem smart to keep debt manageable, this strategy can backfire in the long run, as it often leads to higher overall costs due to interest rates and fees, ultimately prolonging the journey to financial freedom.

Things to Be Aware of:

It’s essential to recognize the hidden costs associated with making only minimum payments. One significant downside is that the majority of the payment often goes toward interest rather than reducing the principal balance, which means the debt can linger much longer than expected. Additionally, relying solely on minimum payments can affect your credit utilization ratio, potentially impacting your credit score negatively if balances remain high. Finally, it can create a cycle of debt dependency, making it challenging to break free and pursue more aggressive strategies for debt repayment, such as consolidating debt or utilizing the snowball or avalanche methods.

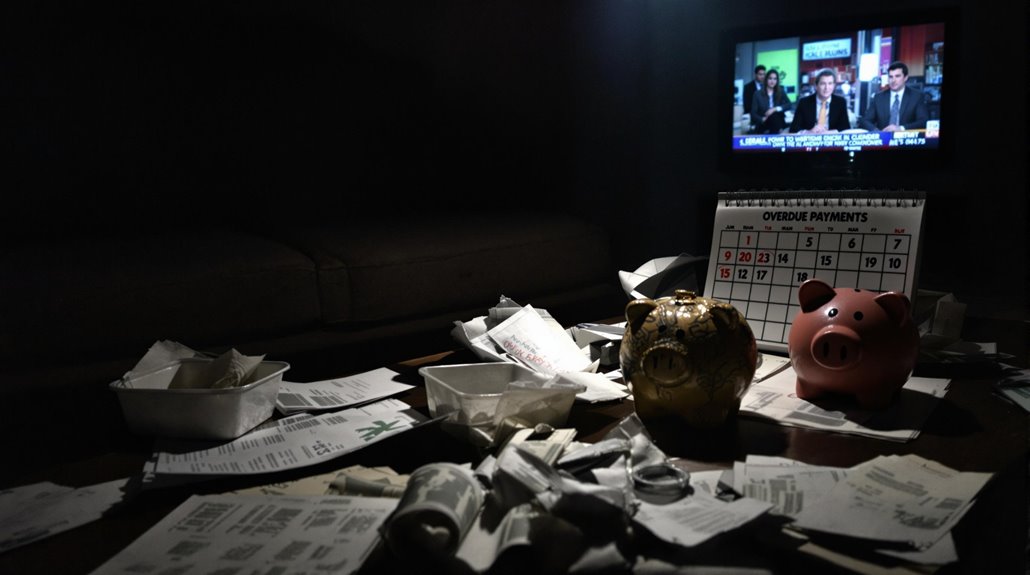

Failing to Create a Budget

What it Looks like: When individuals set out to pay off their debt without a clear budget, the process can quickly become overwhelming and chaotic. They may start by making sporadic payments, focusing on high-interest loans first or tackling smaller debts for a sense of accomplishment. However, without a structured plan, they might overlook important payments, leading to late fees or missed opportunities to consolidate loans. This lack of organization can result in fluctuating balances that are difficult to track, ultimately prolonging the debt repayment journey and increasing stress levels.

Why It’s Smart: Creating a budget is essential for anyone looking to pay off debt effectively. A budget allows individuals to assess their income and expenses, ensuring that they allocate enough funds toward debt repayment while still covering necessary living costs. By identifying areas where they can cut back, such as dining out or subscription services, they can free up extra money to put towards their debts. In addition, a well-structured budget enables individuals to set realistic financial goals, prioritize debts, and monitor their progress over time, ultimately leading to a more disciplined and successful repayment strategy.

Things to Be Aware of: It’s important to recognize that creating a budget is not a one-time task but an ongoing process. As circumstances change—whether due to a raise, unexpected expenses, or changes in living situations—keeping the budget updated is vital. Additionally, some individuals may overestimate how much they can pay off in a month, leading to disappointment or discouragement if they can’t meet those expectations. Maintaining flexibility and being realistic about spending habits can help prevent burnout and motivate continued progress toward becoming debt-free.

Neglecting Emergency Savings

What it Looks like: Neglecting emergency savings while focusing on paying off debt can manifest in several ways. Individuals may find themselves channeling all their extra cash towards debt repayment, leaving little to no funds set aside for unexpected expenses. This approach often leads to a precarious financial situation where even a minor emergency, such as a car repair or a medical bill, can force them to rely on credit cards or loans again. As a result, they may end up in a cycle of debt with no safety net, which can be both stressful and counterproductive.

Why It’s Smart: Maintaining an emergency savings fund while paying off debt is a smart financial strategy for several reasons. First and foremost, having a cushion of funds set aside can prevent the need to accrue additional debt when unforeseen expenses arise. This dual approach allows individuals to tackle their debt while still safeguarding their financial health. Furthermore, an emergency fund contributes to peace of mind, reducing the anxiety associated with living paycheck to paycheck. By balancing debt repayment with savings, individuals can create a more sustainable financial plan that prepares them for both the expected and unexpected challenges life may throw their way.

Things to Be Aware of: It’s crucial to find the right balance between debt repayment and building an emergency fund. While it might be tempting to throw every spare dollar into paying off debt, experts typically recommend having at least a small emergency fund—often suggested to be around $1,000 or enough to cover three to six months of living expenses—before aggressively tackling debt. Additionally, individuals should be aware that neglecting savings can lead to longer-term financial issues, as they may find themselves back in debt if an emergency arises. Creating a budget that allocates funds for both debt repayment and savings can help establish a more stable financial foundation and ultimately lead to greater financial independence.

Using Credit Cards for Everyday Expenses

Things to Be Aware of: However, relying on credit cards for everyday expenses can also lead to significant pitfalls. One major risk is the tendency to overspend, as the ease of swiping a card can detach individuals from the reality of their financial situation. It’s important to keep track of expenditures to avoid exceeding budgets, which can result in accumulating debt that becomes unmanageable. Additionally, if payments are not made in full, interest charges can quickly add up, creating a burden that outweighs any rewards earned. Consequently, while using credit cards can be advantageous, it is vital to approach this habit with caution and a solid repayment strategy.

Not Communicating With Creditors

What it Looks like:

Not communicating with creditors can manifest in various ways. For instance, individuals may avoid answering phone calls or opening letters from their creditors, hoping that the problem will resolve itself. This avoidance can lead to missed payments and increased debt due to late fees and interest charges. Additionally, a lack of communication can result in creditors making assumptions about a debtor’s financial situation, potentially leading to more aggressive collection tactics. The longer one remains silent, the more difficult the situation can become, as creditors may escalate their efforts to recover the money owed.

Why It’s Smart:

On the other hand, maintaining open lines of communication with creditors can greatly benefit those trying to pay off debt. By proactively discussing their financial challenges, individuals may find that creditors are more willing to negotiate terms, such as lower interest rates or extended payment plans. Many creditors have programs in place to assist those facing financial hardship, and being upfront about one’s circumstances can foster goodwill. In addition, consistent communication allows individuals to stay informed about their account status and potential options, helping them make informed decisions that can lead to a more manageable repayment plan.

Things to Be Aware of:

While it’s important to communicate with creditors, it’s equally important to approach these conversations with caution. One should be prepared with all relevant financial information and a clear understanding of their situation before reaching out. Additionally, individuals should be wary of making agreements they cannot keep, as this can lead to further complications down the line. It’s also vital to document all communications for future reference, as this can protect against misunderstandings. Finally, one should be mindful of how they present themselves during these discussions; being respectful and professional can encourage a more positive response from creditors.

Underestimating the Importance of Financial Education

What it Looks like:

Underestimating the importance of financial education often manifests as a lack of awareness regarding basic financial principles. Individuals may believe that simply paying off debt is sufficient without understanding the broader financial landscape that includes interest rates, credit scores, and budgeting. For instance, someone might focus solely on making minimum payments on credit cards, thinking this will suffice to clear their debts, while failing to grasp how accruing interest can extend the life of their debt considerably. Additionally, without financial education, individuals may not recognize the implications of their spending habits, leading to a cycle of debt that is difficult to escape.

Why It’s Smart:

Investing time in financial education is a proactive strategy that can lead to more effective debt management and overall financial health. Understanding concepts such as the snowball and avalanche methods of debt repayment can empower individuals to choose strategies that best suit their financial situations. Furthermore, knowledge of how to improve one’s credit score can open doors to lower interest rates on loans, which can dramatically reduce the cost of borrowing over time. By becoming financially literate, individuals are not only better equipped to tackle existing debts but also to make informed decisions that prevent future financial pitfalls.

Things to Be Aware of:

It’s vital to recognize that financial education is an ongoing process, not a one-time event. Many people fall into the trap of assuming they know enough after attending a single workshop or reading a few articles, but financial literacy requires continuous learning and adaptation to changing economic conditions. Additionally, the sources of financial information can vary widely in credibility; it’s important to seek out reputable resources and consider the advice of qualified professionals. Finally, personal finance is highly individualized; what works for one person might not work for another, so it’s important to tailor financial strategies to fit one’s unique circumstances and goals.

RELATED POSTS

View all